Debt-free living is the path to financial independence. However, do you wish to pay off your loan or mortgage more quickly by making irregular additional payments? Our excel amortization schedule with irregular payments may assist you in resolving your mortgage repayment dilemma in several ways:

- Schedule of amortization with recurring payment (PMT)

- Schedule of amortization with recurring additional payments (Recurring Extra Payment)

- Amortization plan with irregular additional payments (Irregular Extra Payments)

- Allow me to demonstrate how to use this template.

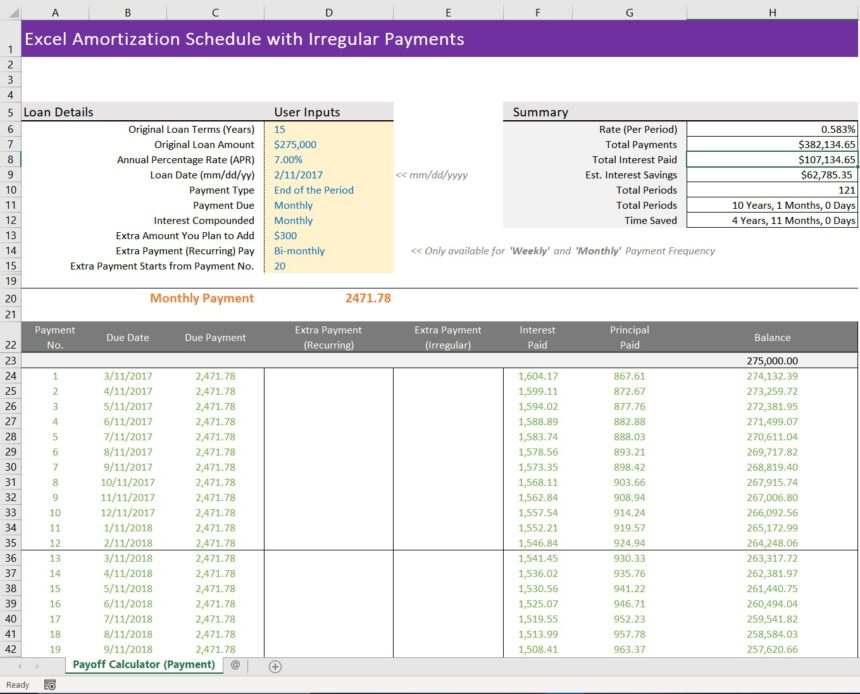

Suppose you get a mortgage loan (or loan for any other reason) with the following terms:

- Loan Quantity: $275,000

- Loan Conditions: 15 Years

- 7 percent Annual Percentage Rate (APR)

- Type of Payment: End of Period

- Monthly Frequency of Payment

- You want to determine your monthly payment amount.

Observe the picture with attention.

1) Your monthly obligation will amount to $2471.78.

2) On the right side of the picture, you’ll see information on your loan. Total amount payable (principal plus interest) = $382,134.65

Total interest payment = $107,134.65, and you did not save any money since you just made the minimum monthly payment.

3) The amortization table is shown in the bottom portion of the picture. The green numbers in the amortization table represent the periods for which you have (or should have) completed your payments.

Excel Amortization Schedule With Irregular Payments

Now that twenty payments have been paid, your monthly income has risen. Therefore, you want to make additional recurring payments to your monthly payment beginning with the twenty-first period.

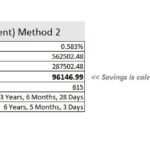

Suppose you want to pay an additional $300 every two months for the remainder of the loan’s term. I just entered this data into the template, and the results are shown below.

1) We have included the information shown above. Extra payment = $300. Each further payment will be made every two months. Therefore, I picked Bimonthly from the drop-down menu. The additional payment will begin with the twenty-first period.

2) Review the loan overview on the right. Your new total payment (principal plus interest) is $382,134.65 Total interest payment = $107,134.65 and you will save a total of $62,785.35. Fifteen years have been reduced to 10 years, one month, and zero days.

3) The amortization chart reflects the additional bi-monthly payment beginning with the twenty-first period.

Terms Used In Excel Amortization Schedule With Irregular Payments

As stated in its original terms, the total amount of time allotted to repay the debt is expressed in years. This tenure period might span from 15 to 30 years for residential mortgages. This period might span anywhere from three to five years for auto loans.

The first sum you are taking out as a loan from a financial institution is the “Original Loan Amount.”

APR stands for annual percentage rate. This kind of interest rate is sometimes referred to as a nominal or stated interest rate. This is the interest rate shown on the paperwork for your loan. However, your annual percentage yield is different from the stated rate.

Types of Payment: Payment types are two possible times: at the end of the period (which is the more common option) or at the beginning of the period. Both of those options are available to you in this model.

Payment Due: It is the frequency of the payments. How many payments do you anticipate making in a single year? The majority of mortgage loans include monthly payments. However, you can choose various payment frequencies (table below). The drop-down menu provides options for all of these different payment frequencies.

The compounded interest amount often corresponds to the amount paid regularly. For example, if your payment schedule is every month, the interest will likewise be compounded. Even if payments are made every month in certain countries, such as Canada, the interest may only be compounded every six months. Learn how to handle situations like that by reading the article linked here. Take a look at this article’s intriguing title: What happens if payments are made every month, but interest is compounded on a semi-annual basis?

The meanings of the other choices should be obvious. For example, extra Amount You Plan to Add, Extra Payment (Recurring) Pay, and Extra Payment Starts from Payment No. are the names given to these three options.

Factors To Keep In Mind For Excel Amortization Schedule With Irregular Payments

1) Does your financial institution impose a fee for early loan repayment?

Some financial institutions may impose a prepayment penalty. In this scenario, you will be required to pay a prepayment penalty to get out of the mortgage loan early. Because of this, I strongly suggest that you investigate the loan’s terms and conditions before agreeing to it.

2) Do you currently have any high-interest CREDIT card debt or vehicle loans?

Mortgage loans provide the industry’s most competitive interest rates. Therefore, if you have any high-interest loans, such as credit card debt, auto loans, or any other kind of high-interest loan, please pay them off first. Then you should think about paying off your mortgage debt.

The interest rates on vehicle loans and credit cards are often much higher than those on home loans. Therefore, you should make payments to them first before paying off your home debt.

3) Do you have enough money stashed away in your emergency fund?

Did you save 3-6 months’ spending on your emergency fund? Your expenses for the next three to six months can be covered by an emergency fund that is completely funded. However, if your emergency fund is not nearly enough to cover the situation, you should prioritize saving money for it.

Conclusion

I hope that our excel amortization schedule with irregular payments will prove to be of great use to you while you are calculating the amortization of your mortgage. In the comment box, please let us know if you have any criticism or if you would want any more features added to this template. I hope you never have to deal with debt again.